I want to talk with you today about Health Insurance. And I want to talk to you about it for several reasons, namely it’s expensive and has hit some snags this past year in terms of online enrollment. But also I want to help you avoid becoming lost in those online snags by listening to my own struggle and how I was eventually able to understand a system that doesn’t really understand itself. Open enrollment is coming up and I can bet a great number of you reading this will need to renew or reapply. Maydad Cohen, Special Assistant for Project Delivery to Massachusetts Governor, Deval Patrick, recently released “Why the Mass. Health Connector Website Will Work”. But the article’s attempts to provide reassurance through hard data really didn’t provide the kind of data you’ll need to navigate the fires they are already trying to put out. So what is open enrollment and what does that mean for you in terms of stress and time? Well let’s talk about that, and how you can best be prepared to navigate the health insurance exchange in Massachusetts.

In October of 2013 I was signed up for a subdivision of Mass Health, the government-sponsored organization that provides health insurance at various rates for those that are not making a lot of money. I was working three part-time jobs, none of which provided health insurance. At that time, I paid $81 a month for coverage. In June of 2013, a letter showed up on my doorstep telling me I’d been terminated from my entire plan, and all coverage would stop at the end of the month. Had I known then what I know now, I may have had the smarts to better fight the system and correctly get myself reassigned to a different plan. What I’m going to say may be that game-changer for you and a lifeline so please listen up.

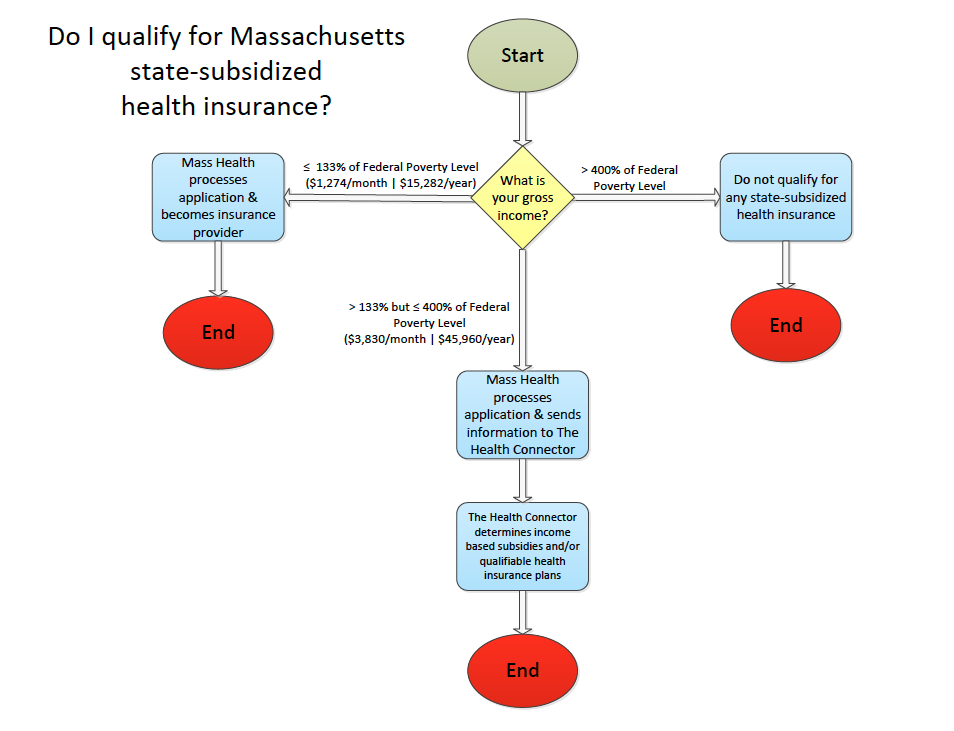

To understand the way the health insurance system in Massachusetts recently faltered, we have to understand how it was put together. Now there are two organizations that ideally work together to make sure that those making under $45,000 annually get help with their health insurance bills (please see MassResources.org for all figures, available online). These are Mass Health and The Health Connector. When you fill out your application, you are sending that information to Mass Health. And this is all about income, friends. So the first thing we need get straight is this- how much do you make?

Adjusted Gross Income (henceforth AGI) is a term you need to know. This is how much you make per year before taxes are taken out. That amount is key, and it is the amount that Mass Health pays attention to when you apply. Now to be concise, if your AGI is at 133% of what’s called the Federal Poverty Level (FPL), then you can absolutely have Mass Health. The Federal Poverty Level is the amount of gross income a family or individual must make every year to be considered unable to pay for necessities like food and shelter. (The Institute of Research on Poverty). It’s issued every year by the Department of Health and Human Services and is important for us because it’s what determines if the government is going to help you with your insurance. Per MassResources.org 133% of the FCP correlates to $1274 a month prior to taxes. Make any more than that and your application is going to travel from Mass Health to the Health Connector.

Still with me?

To reiterate, should you make more than $1274 per month, your application will be en route to the Health Connector. At the Health Connector, some bright young person is going to say “Alright. Well George makes more than 133% of the federal poverty level, but does he make less than 400%?” <– See that number- 400%? That is the cut off. If you annually make less than $45,960 aka 400% of the Federal Poverty Level you should qualify for what are called subsidies for your health coverage. In other words, the government will help you pay for your insurance in some way depending on your income. For those that are more visual (myself included) here’s a look at a graph to better show the process:

Values derived from MassResources.org.

Values derived from MassResources.org.

So now that we know how much we need to make (or not make) to get government help with our insurance, I want to tell you what happened to the health insurance enrollment system and how that may affect you. We’re about to lay out our offense and our defense, so get those ears perked up!

The insurance I was on when I was kicked off was a division of a now inoperative branch of the Massachusetts Health Insurance system called Commonwealth Care. Though it has since been absorbed into the Health Connector and is no longer in operation, it was a program that served those who made too much to be on Mass Health (above 133% of the FPL), but not enough to afford privatized insurance (less than 400% of the FPL). Mass Health was in charge of both companies. When I was kicked off in June of 2013 there was a monetary difference I had made over a couple of months from an additional job. This meant that I was making $300 too much per month to stay on my current plan. What Mass Health did not pick up on was that after handing in a new pay stub, I still absolutely qualified for health insurance. So what happened there?

In Massachusetts, when you leave or are kicked off of your insurance you have 65 days to find another insurance company or you cannot sign up for coverage until the next Open Enrollment Period. An Open Enrollment Period is a time period of a couple months when the Government says “Hey everybody, NOW you can sign up!” The issue? This happens once (yes, I just said ONCE) a year. Open Enrollment Period is scheduled to begin this November and extend through February. Why am I telling you all this? You need to get yourself in gear as it’s around the corner.

After being kicked off, I realized fairly quickly that no one was going to let me have insurance as the time it took me to contest my termination took longer than 65 days. I was removed from my insurance in June of 2013 and had to wait until the open enrollment period that Fall to reapply. My new application was submitted at the beginning of November (6 months without insurance at that point). I even went to what’s called a Navigator Agency to help me, which is an organization designed to help the general public complete applications.

Now at that time the rollout of the Affordable Care Act was taking place across the country. Signed into law in 2010, The Affordable Care Act, aka Obama Care, is a system of reforms designed to make sure more Americans have health insurance, even if they have pre-existing conditions or aren’t making much money. Per Healthinsurance.org, “Key provisions are intended to extend coverage to millions of uninsured Americans, to implement measures that will lower health care costs and improve system efficiency, and to eliminate industry practices that include rescission and denial of coverage due to pre-existing conditions”. Unlike other states, Massachusetts already had mandated health insurance for years and because of this had a preexisting online enrollment system. General thought therefore was that the state would somewhat easily adopt the new system that catered to the needs of the Affordable Care Act. But while the adoption of a brand new system in many states went off without many hitches, in Massachusetts it sank like a stone. Here is why:

Beginning in the early 2000’s, Massachusetts used an online application website called Virtual Gateway (“How Louis Guitierrez Helped Implement a Virtual Gateway for Mass. Dept of HHS”). While somewhat archaic, the program worked. However, after the Affordable Care Act rolled out, MA’s answer to accommodate it was called the Health Insurance Exchange- aka the HIX system. The issue? In layman’s terms the HIX system didn’t work. Through a reference of mine I learned that the very people certified to help the public get health insurance were also misinformed of the system’s cracks. Per my source,

The system seemed like it would be better than what currently exists, it was going to be launched flawlessly, and it wasn’t until about a week after the official launch that it became apparent there were serious bugs or serious problems with the system. And they had to have known that there were problems beforehand.

So what do you do when an online application program is falling apart? Go back to paper. Long, tedious, paper applications. Many times, paper was used in addition to “successful” online applications, simply because it could not be guaranteed that online applications were going through. Paper applications take approximately four times longer to complete. Imagine the family with the five kids who all need to apply together for minimally an hour filling out paperwork. Now imagine the waiting room.

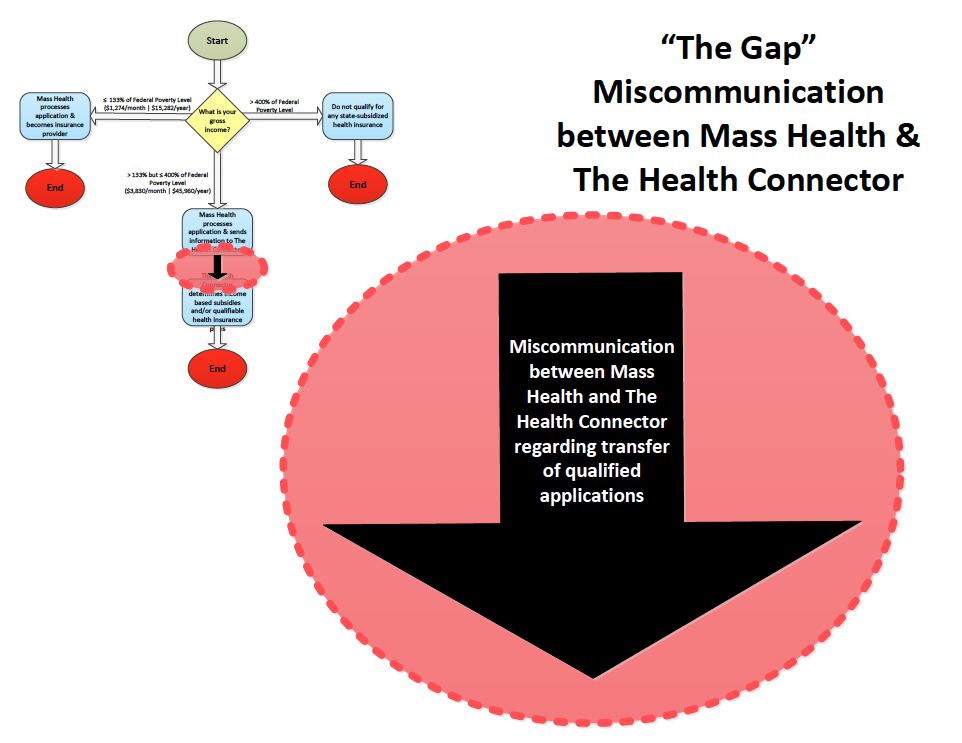

Applications were coming in and needed to be processed, but 50,000 of these applications got stuck, and here’s how (Michael Levenson,“50,000 Filings for Health Insurance in Limbo,” Boston Globe): Once applications are sent to Mass Health, paper or otherwise, they are to be processed within 45 days (MassResources.org). You are to be given an answer in that period to ensure you still have time to apply elsewhere if needed. But the HIX system couldn’t get applications processed properly, and in addition there was gross miscommunication between Mass Health and the Health Connector- our two organizations that need to talk to each other to get your application handled. Many found their applications lost to what I call the “Gap”. The Gap is the area of free fall where for various reasons applications were lost, put aside, or mishandled. The organizations failed to communicate with one another and subsequently struggled with how to handle so many applications they could not process on time if at all. For a visual:

Depending what organization you called to follow up with your application- Mass Health or the Health Connector- you could get wildly different answers. Both organizations’ employees were egregiously misinformed of how their company was (or was not) operating at that time and so inundated with calls, you simply could not reach a person. 25-minute holds were commonly disconnected by an automated system. The Navigator Agencies, designed to be the public’s insurance helpers, could do no better with the tracking of submitted applications.

My case was particularly wild because no one seemed to understand that my new application was not the same file that Mass Health previously terminated. Every phone call inevitably had an agent telling me something different, depending on whether they were able to differentiate that I had reapplied. Some answers were:

*”You aren’t eligible, you were terminated already.”

*”We see you do have insurance, you need to speak to a Supervisor.”

*”We see you filed an application, we don’t know yet if you have the coverage but your temporary ID should work.”

Two items to chat about for a moment- supervisors and temporary ID’s. I did in fact receive two phone calls from Mass Health “supervisors” telling me that I did have health insurance and to call them back. One major problem? The phone number they provide should you miss the call (I did) goes to the primary help line. The agents at the primary help line are “not allowed” to let you speak to a supervisor, and simultaneously could not determine whether I had health insurance. It was just the worst catch 22.

Now this temporary coverage- it’s important. Around January of 2014 when it was pretty obvious things weren’t going as planned, Mass Health began sending out letters telling anyone who had applied that they would be covered by the state until this whole mess could be figured out. For some people, that worked. For me, a number I was provided to give to doctors and pharmacists to cover visits and prescriptions, was linked to my terminated account, not my new application. So it did absolutely nothing.

At this point, it’s January, 2014 and I haven’t seen a doctor in 7 months. I have a medical condition requiring me to see a doctor about every 4 months, so this wasn’t going to work out. After many exchanges with employees at the Navigator Agency, countless calls to Mass Health and the Health Connector, I realized very clearly I was on my own. I had to buy private insurance and I had to buy it before the end of that enrollment period. So I got one of the less expensive ones at $358 a month. Can I afford this? Not particularly, but I try to be very careful.

When my private insurance kicked in, it was March. I hadn’t been to a doctor in 9 months. During all this time, and currently, I receive letters in the mail written sometimes months prior to their postmark telling me I still have temporary coverage from Mass Health. This apparently will continue to December of 2014 as the system’s errors are not yet rectified. In early August after the most recent of these letters, I made calls to both the Health Connector and Mass Health. The Health Connector incorrectly informed me that the reason I still didn’t have Mass Health Coverage was because I had bought my own insurance, voiding a necessity for me to need any in “The System”. And maybe if I canceled that I would have Mass Health Coverage.Should anyone say something similar to you, the answer is that that is not true. A subsequent call to Mass Health told me that in fact that I DID have Mass Health coverage (after all this time, I have no idea how) and that they would then function as my secondary insurance. This is a fact many people don’t know about, and one I wouldn’t have known had I only called the Health Connector.

So as you approach November’s enrollment period, there is a very real possibility that this system will not be fixed, despite Cohen’s earlier reporting of the millions poured into the IT revamp of the website. Let’s cut the baloney and say this- I am an educated person who speaks English fluently who had help at a Navigator Agency, and I still could not gain ground. Can you imagine how families with who may or may not speak English well are doing? As my reference told me,

There is one shot to do [the application] right. Because we might lose them, they might fall through the cracks… and you can’t do that to people who have a busy lifestyle where they have, you know, two minimum-wage jobs and a family to raise, or there may be a communication barrier.

Massachusetts’ health insurance enrollment system has faltered a bit, despite being designed to assist a National health insurance law that in many ways has proven exceptionally helpful to many in need. And while the state has made strides getting many of its residents insured, many were left unfortunately uninsured for extended periods of time. So I don’t want you to fall into that Gap, and I don’t want you to be alone. When you go in, know how much you are making, and based off of this know where your application SHOULD be going. Be prepared with that knowledge. We’re currently in a much better place than we were one year ago, and knowing where you stand will help you on your way to your new insurance this fall.